View a French translation of this blog post.

Madeleine, the President of one of Yikri Burkina Faso’s microfinance groups, has successfully taken business loans to support livestock rearing activities. However, when explaining the difference the Yikri program had made in her life, she first recounted not the impact of credit on her economic situation but the importance of the savings accounts Yikri provides.

Launched by the French network Entrepreneurs du Monde, Yikri is one of Whole Planet Foundation’s microfinance partners, part of a network we work with all around the globe to fund microcredit to the world’s poor. Although Whole Planet Foundation provides capital to finance microloans to entrepreneurs in poor communities around the world, we know credit is only one part of a complex financial support system that can improve the lives of poor households.

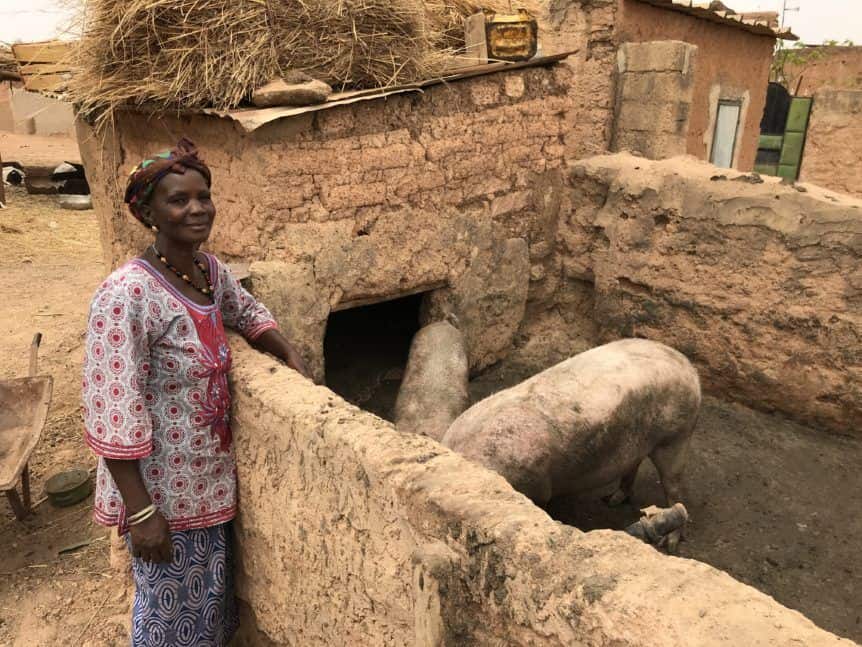

Madeline raises pigs with a microloan from Yikri in Burkina Faso. Photo: Brian Doe

Prior to joining her Yikri group, Madeleine participated in a traditional savings scheme within her village where savings are collected and kept by a member of the community. One day, she lost everything she had saved when that collector’s house burned down. After that experience, she remembered trying to save her money with a local savings and credit company that ended up going out of business and ultimately paid out a fraction of the money she had saved at the institution over time. Despite how successful her enterprise was, she found herself back to zero economically because she couldn’t reliably save for the future and build the funds she needed to to cover larger investments in her business and household.

Research into the impact of the microcredit sector has shown that stand alone, ‘one size fits all’ microlending programs are not as effective as those that provide credit flexible to borrowers’ needs. Flexible business loans layered with easily accessible savings services, training, and when possible, more advanced products like insurance and asset leasing have more potential for sustainable economic empowerment of the poor.

The Harvard Business Review wrote in 2016 to highlight this research: “Recent evidence suggests that relatively simple tweaks to microcredit products—including flexible repayment periods, grace periods, individual-liability contracts, or the use of technology—may change their impact on poverty and financial institutions’ bottom line.”

Having just returned from a visit to Burkina Faso to observe the operations of WPF’s partner Entrepreneurs du Monde, no organization seems to have been so responsive to these recommendations. Entrepreneurs du Monde through their ‘Yikri’ microfinance program does provide microloans to thousands of micro-enterprises in Burkina Faso (and other countries) but every enterprise supported is assessed independently and the repayment period is set up in collaboration with the entrepreneur to be appropriate to the business activity. Loans can vary from 3 months to 12 months and there is a possibility for a grace period until the end of the loan if the business activity necessitates it (such as Madeleine’s livestock activity that takes time to realize a profit).

A photo of Madeline during her loan group meeting. Photo: Brian Doe

Additionally, every client is provided a savings account and encouraged to save for future needs and is also able to withdraw funds whenever necessary. While clients meet with their loan officer in groups with other borrowers, the liability for the loans is completely individual, with groups serving solely as a platform to reimburse, save, and access Entrepreneur du Monde’s 34 different training modules. These modules range from financial literacy to business skills. Groups can participate in trainings on subjects like: strategies for increasing profit margins, starting a new business, and overcoming volatility in energy access and costs.

In many countries, local regulations make it very difficult for socially-minded financial service providers to offer more than just microloans, even if they would like to expand services to their clients. The methodology Entrepreneurs du Monde is expanding is both expensive and labor intensive, and Entrepreneurs du Monde in Burkina Faso is still working to scale to a size that can show its model can break even in a country with high operating costs and logistical challenges (plus mandated caps on the fee they can charge for their services which is lower than surrounding regions). The program has only just begun to reach into rural areas outside the capital which will prove even more difficult to serve in a cost effective way.

However, if more microfinance institutions can expand access to more diverse and tailored services, the benefits can be great. Hopefully more countries can increase incentives to microfinance institutions to encourage them to expand the services they offer. Whole Planet Foundation has supported Entrepreneurs du Monde affiliates in Cambodia, Togo, Ghana, India and the Philippines.

Invest in a future without poverty! Help us fund a microcredit loan annually in the Sub-Saharan Africa region for $10 a month as part of our Explore+Invest monthly donation program.