In March, I wrote the blog Whole Planet Foundation and Microfinance Partners Respond to the COVID-19 Crisis around how those living in poverty are already in a more vulnerable position, which can be further exacerbated during any external shock such as war, earthquakes, droughts or health crises.

Seven months into this global pandemic, I want to provide an update on COVID-19’s ongoing impact on the microentrepreneurs we support, how microfinance organizations (MFIs) are coping, and our team’s shift to remote work.

Photo at the top of this post courtesy of BRAC Tanzania: BRAC Tanzania staff handle disbursement activities with caution during the COVID-19 pandemic.

Across the world, vast numbers of people have lost their jobs or seen their incomes fall. According to the UN World Food Program’s 2020 Global Report on Food Crises, the COVID-19 pandemic could see more than 250,000,000 people suffering acute hunger, while up to three dozen nations could face famines by the end of the year, potentially pushing an additional 130 million people to the brink of starvation.

Many are being forced to sell the few assets they have in order to cover consumption needs. Ideally, government safety nets would help plug such financial gaps, but in many countries, governments do not have the resources or ability to distribute cash transfers that would help pump vast amounts of money to sustain crippled economies. Microcredit, a form of lending tailored to the most vulnerable or for those living in very remote and rural communities has been part of the answer, but the sector is facing challenges as well.

Microfinance partner, Sembrar Sartawi, in Bolivia offers hand sanitizer to a member in the branch office

COVID-19’s Impact on Microcredit Clients

The capacity of a client to repay his or her loan has been affected by many different factors, including business closures or slowdown, operational difficulties or regulatory prohibitions on holding large meetings or limits on public transportation preventing staff or clients to meet. Client repayments, usually done in cash and in weekly group meetings, have plummeted following COVID-related restrictions, yet the banks and investors which provide the MFIs with funds still expect to be repaid. A crunch was on the horizon through most of Spring 2020. In the short term, viable MFIs needed additional support from donors and investors through debt repayment moratoriums, rescheduling or injecting more capital to smooth cash flows.

Microfinance Institutions Respond

Back in June, we wrote about the early results of lender groups in The Pledge to Protect Microfinance Institutions and Their Clients From the Economic Effects of COVID-19, outlining the impact of such discussions. WPF joined the pledge of Key Principles, aiming to help build momentum for a toolbox that participating investors are using to collectively help microfinance institutions survive this crisis and to be well positioned to quickly bolster entrepreneurs’ businesses once COVID-19 lockdowns are eased. The first objective was to create an open dialogue between lenders to collectively work to ensure capital stays with the microfinance institutions that all are seeking to support. While many MFIs paused loan disbursements during this time, it was vital that when restrictions were lifted, the MFI would have the capital to offer fresh new loans to provide relief funding and help jumpstart clients’ businesses.

Branch staff of KOMIDA in Indonesia prepare COVID19 relief packages for their members.

As client repayments have plummeted, the other main risk facing many MFIs is their portfolio quality. PAR30 (loans repayments that are more than 30 days late) is the most common indicator of how an MFI’s portfolio is performing, and we see some warning signs emerging across many of our historically strong partners. However, it’s important to note that at least part of the increase is likely due to declining portfolio growth. A growing portfolio can mask underlying weakness. When growth stops or reverses, PAR levels increase, and that’s one likely driver of the April/May spike we’re seeing in our quarterly reporting from our partners.

Moreover, loan restructuring and repayment suspensions add to the uncertainty. As CGAP highlights in their CGAP Global Pulse Survey of Microfinance Institutions:

- PAR30 levels do not solve the portfolio quality puzzle by themselves. Write-offs also are important to consider but given their lagging nature we are setting them aside for now. More significant in the case of the pandemic are the loans that have been restructured, including those restructured as a result of COVID-19 moratoria on principal and interest that have been mandated by governments or voluntarily provided by MFIs.

- Our data show extremely high levels of restructured loans. We can add those restructured loans to PAR30 to arrive at a figure we can call “troubled portfolio,” which reached nearly 50 percent among our respondents by the end of May 2020. These troubled portfolios are the gathering clouds in our analogy. We see them at a distance, but whether they will cause a storm and how much damage that storm would inflict depends on several factors. The uncertainty is especially pronounced among the loans that are subject to moratoria; we simply do not know how those loans will perform.

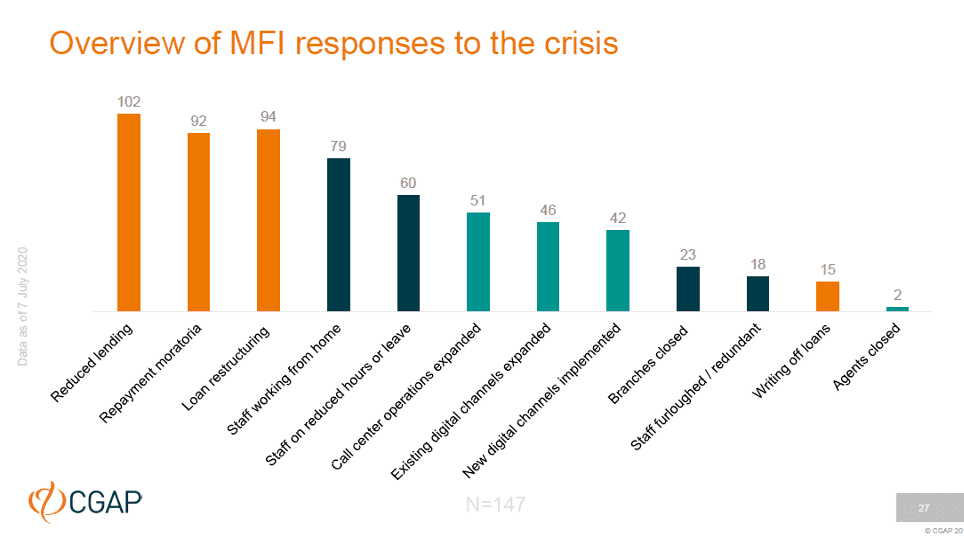

Moreover, the CGAP pulse survey collected COVID relief and responses from their 147 participating MFIs.

This analysis aligns with our own surveys and reporting with WPF-supported MFIs. Over the next few weeks, we will be publishing a series of blogs from the WPF field team which will expand on COVID-specific innovations in technology as well as some specific examples of how our partners have responded to the current crisis and continue to provide valuable products and services to their members.

We have seen the pandemic as an accelerator of technologies used to implement/operate microcredit. Like so many other industries, those with technologies in place were able to quickly respond to market changes and emerging opportunities. Those in the process of digitizing were forced to accelerate the adaptation and those which have been reluctant to improve their information systems and operating methodologies are proving to be far less resilient.

Whole Planet Foundation’s Remote Response

Given the support we have from Whole Foods Market, WPF is fortunate to be able to visit every active partnership annually. This has allowed the Foundation to build a nuanced perspective of how these institutions operate and their unique vulnerabilities. We see this in-depth perspective as invaluable for the responsible management of donor dollars. However, while travel restrictions remain in most parts of the world, we have shifted to a remote review process which includes:

- Quarterly metrics review – Gathering partner outreach and portfolio quality data and comparing actuals against project targets.

- Covid19 Response update /delinquency management –We assume a strong correlation between the two and seek to understand how each partner is responding both to the health crisis and economic restrictions. Our priority is ensuring procedures for client protection in the context of COVID nonrepayment remain intact.

- Senior Management Discussion –Teleconferencing with heads of departments (Finance, Operations, HR, Internal Audit, Social Performance Management, Systems).

- Financial Review and analysis – Compiling both financial and operational key performance indicators to understand historic trends.

- Operations review –When possible, teleconferencing with branch manager or field officer. We also collect photos/copies of client passbooks, client repayment schedules, and client loan contracts.

We use this information to assess the risks facing each of our partners and determine when WPF authorized funding should be released or delayed based on their lending capacity. Moreover, how we can respond to partner needs such as expediting funds to contribute to partners recovery loan products or expand project areas to allow for increased flexibility.

As we continue to track the impact of COVID-19, the following table shows the movement of risk across our MFI partners:

| 2020 – Risk Assessment Summary | April 1st | July 1st |

| MFIs partners in a strong position | 35 | 19 |

| Midterm vulnerability | 44 | 50 |

| Immediately vulnerable | 4 | 8 |

| High Risk | 2 | 5 |

Though we have adjusted our approach, we continue to do all we can to monitor and evaluate the changing landscape, especially as the risks increase for the very poorest and for our trusted partners. In these uncertain times, our programmatic objective continues: to allocate WPF funding in the most impactful way, driven by data and customer obsession.

We look forward to sharing more on our experiences and observations through the upcoming COVID-19 Response blog series.